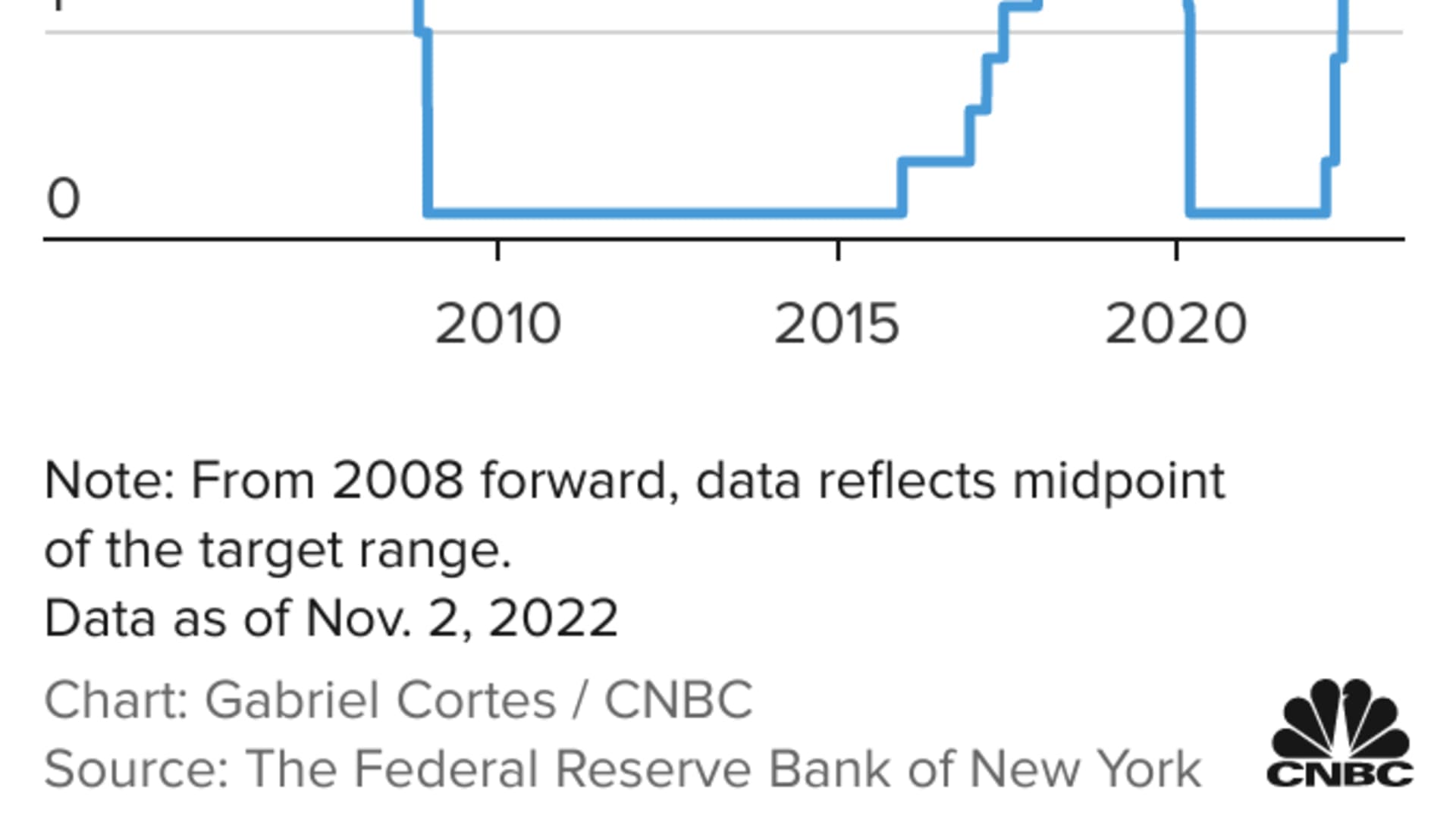

- The Federal Reserve, in a well-telegraphed move, raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

- The central bank's new statement hinted at a potential change in how it will approach monetary policy to bring down inflation.

- However, stocks fell as Fed Chair Jerome Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

- Still, Powell reiterated that there may come a time to slow the pace of rate increases.

The Federal Reserve on Wednesday approved a fourth consecutive three-quarter point interest rate increase and signaled a potential change in how it will approach monetary policy to bring down inflation.

In a well-telegraphed move that markets had been expecting for weeks, the central bank raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high.

Along with anticipating the rate hike, markets also had been looking for language indicating that this could be the last 0.75-point, or 75 basis point, move.

The new statement hinted at that policy change, saying when determining future hikes, the Fed "will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments."

Economists are hoping this is the much talked about "step-down" in policy that could see a rate increase of half a point at the December meeting and then a few smaller hikes in 2023.

Changes in policy path

This week's statement also expanded on previous language simply declaring that "ongoing increases in the target range will be appropriate."

The new language read, "The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time."

Money Report

Stocks initially rose following the announcement, but turned negative during Chairman Jerome Powell's news conference as the market tried to gauge whether the Fed thinks it can implement a less restrictive policy that would include a slower pace of rate hikes to achieve its inflation goals.

Get a weekly recap of the latest San Francisco Bay Area housing news. >Sign up for NBC Bay Area’s Housing Deconstructed newsletter.

On balance, Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

He also reiterated that it may take resolve and patience to get inflation down.

"We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected," he said.

Still, Powell repeated the idea that there may come a time to slow the pace of rate increases. He has said this at recent news conferences

"So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made," he said.

Soft-landing path narrows

The chairman also expressed some pessimism about the future. He noted that he now expects the "terminal rate," or the point when the Fed stops raising rates, to be higher than it was at the September meeting. With the higher rates also comes the prospect that the Fed will not be able to achieve the "soft landing" that Powell has spoken of in the past.

"Has it narrowed? Yes," he said in response to a question about whether the path has narrowed to a place where the economy doesn't enter a pronounced contraction. "Is it still possible? Yes."

However, he said the need for still-higher rates makes the job more difficult.

"Policy needs to be more restrictive, and that narrows the path to a soft landing," Powell said.

Along with the tweak in the statement, the Federal Open Market Committee again categorized growth in spending and production as "modest" and noted that "job gains have been robust in recent months" while inflation is "elevated." The statement also reiterated language that the committee is "highly attentive to inflation risks."

The rate increase comes as recent inflation readings show prices remain near 40-year highs. A historically tight jobs market in which there are nearly two openings for every unemployed worker is pushing up wages, a trend the Fed is seeking to head off as it tightens money supply.

Concerns are rising that the Fed, in its efforts to bring down the cost of living, also will pull the economy into recession. Powell has said he still sees a path to a "soft landing" in which there is not a severe contraction, but the U.S. economy this year has shown virtually no growth even as the full impact from the rate hikes has yet to kick in.

At the same time, the Fed's preferred inflation measure showed the cost of living rose 6.2% in September from a year ago – 5.1% even excluding food and energy costs. GDP declined in both the first and second quarters, meeting a common definition of recession, though it rebounded to 2.6% in the third quarter largely because of an unusual rise in exports. At the same time, housing demand has plunged as 30-year mortgage rates have soared past 7% in recent days.

On Wall Street, markets have been rallying in anticipation that the Fed soon might start to ease back as worries grow over the longer-term impact of higher rates.

The Dow Jones Industrial Average has gained more than 13% over the past month, in part because of an earnings season that wasn't as bad as feared but also due to growing hopes for a recalibration of Fed policy. Treasury yields also have come off their highest levels since the early days of the financial crisis, though they remain elevated. The benchmark 10-year note most recently was around 4.09%.

There is little if any expectation that the rate hikes will halt anytime soon, so the anticipation is just for a slower pace. Futures traders are pricing a near coin-flip chance of a half-point increase in December, against another three-quarter point move.

Current market pricing also indicates the fed funds rate will top out near 5% before the rate hikes cease.

The fed funds rate sets the level that banks charge each other for overnight loans, but spills over into multiple other consumer debt instruments such as adjustable-rate mortgages, auto loans and credit cards.